Non Allowable Expenses For Corporation Tax Malaysia : However, the allowable expenses under subsection 33(1) of the ita is subject to specific prohibitions under subsection 39(1) of the ita.

Non Allowable Expenses For Corporation Tax Malaysia : However, the allowable expenses under subsection 33(1) of the ita is subject to specific prohibitions under subsection 39(1) of the ita.. A company or corporate, whether resident or not, is assessable on income accrued in or derived from malaysia. (b) direct expenses incurred in the letting of real property by unit trusts other than reits/ptf where the income from the letting of property is charged to tax under section 4(d) of the ita 1967. Individual carrying on a business on his own. With effect from (w.e.f) year of assessment (ya) 2008, a labuan entity can make an The expenses wholly and exclusively incurred in the production of the rental income are allowable as a deduction to.

After deducting all business losses, allowable expenses, approved donations and personal. As such, there's no better time for a refresher course on how to lower your chargeable income. Corporate tax malaysia 2020 for smes comprehensive guide biztory cloud accounting. Chapter 5 corporate tax stds (2) 1. This expenditure is usually referred to as 'wholly & exclusively'.

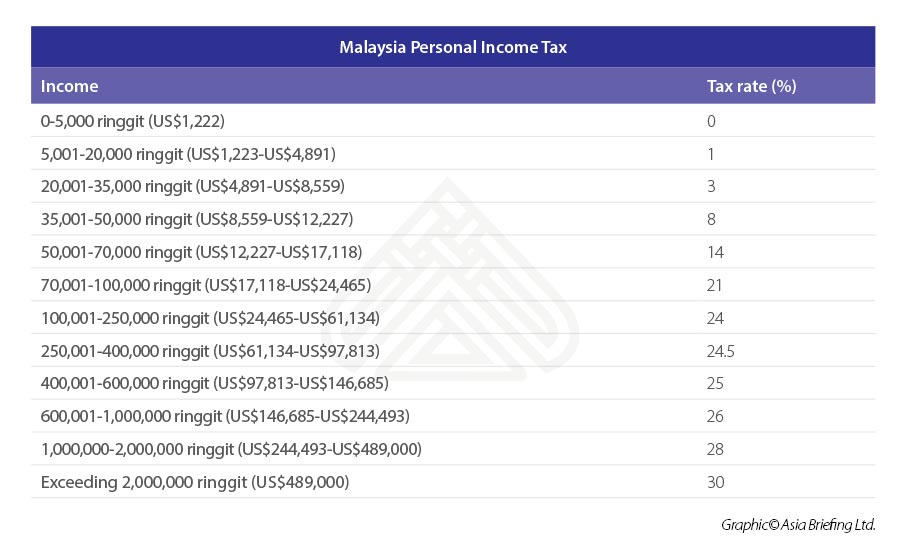

Individual Income Tax In Malaysia For Expatriates from www.aseanbriefing.com Although tax rates may vary based on yearly budget announcements, corporate income tax must be submitted and filed on a yearly basis, similar to an individual's personal income tax. For more information and source,. For more information and source, see on this link : A malaysian company can claim a deduction for royalties, management service fees, and interest charges paid to foreign affiliates, provided that these are made at arm's length and the relevant whts, where applicable, have been deducted and remitted to the malaysian tax authorities. On the chargeable income exceeding rm 600,000. For more information and source, see on this link : An easier way to remember what is allowable is to use the tax return itself. Legal fees are usually allowable and this includes costs of chasing debts defending trademarks preparing legal agreements.

For example, the cost of hiring domestic servants to help in housekeeping while one is away at work is not deductible.

On the first rm 600,000 chargeable income. A company or corporate, whether resident or not, is assessable on income accrued in or derived from malaysia. On the chargeable income exceeding rm 600,000. For more information and source, see on this link : Business expenses allowable vs st partners plt chartered accountants malaysia facebook. Gains or profits from carrying on a business, trade, vocation, or profession are liable to tax. Disallowable deductions expenditure which is not wholly and exclusively intended for trade purposes, is not allowable. Corporate tax malaysia 2020 for smes comprehensive guide biztory cloud accounting. The advance rental would be taxed in the year of receipt. After deducting all business losses, allowable expenses, approved donations and personal. For more information and source,. Expenses on repairs and renewals generally, repairs and renewals expenses are claimed as deductions from a person's gross income from a business or rental source. But in malaysia, it's a bit different.

List of non allowable expenses in malaysia 2018. In short, when you spend money to earn money, you're allowed to deduct that cost from the. The expenses must be incurred. However, the allowable expenses under subsection 33(1) of the ita are subject to specific prohibitions under subsection 39(1) of the ita. Expenses on repairs and renewals generally, repairs and renewals expenses are claimed as deductions from a person's gross income from a business or rental source.

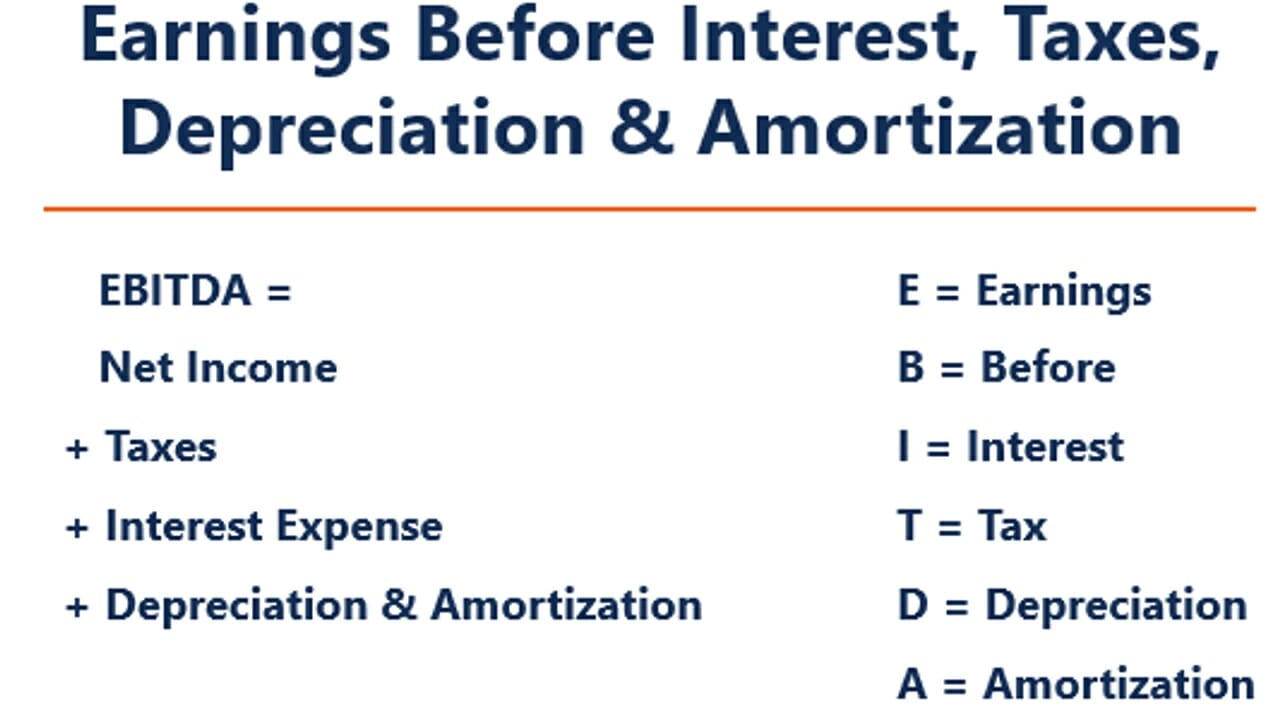

What Is Ebitda Formula Definition And Explanation from cdn.corporatefinanceinstitute.com Typically, initial expense is not allowed a deduction from income of letting of continue reading →. Generally, you are only taxed for the profit that you or your business earns. As such, there's no better time for a refresher course on how to lower your chargeable income. Chapter 5 corporate tax stds 2. For more information and source, see on this link : Non allowable expenses for corporation tax malaysia. To subsidiary or headquarters to branch in malaysia overseas trips 40 housing developers 40 transfer pricing 41 Application of tax law 6.1 generally, expenses incurred by a person prior to the commencement of his operations or business would not be allowable as a deduction against the gross income of his business as they are not wholly and exclusively incurred in the production of the income.

For more information and source, see on this link :

• to determine the gross income of a company (business and non business) to identify deductible expenditure to compute the chargeble income of a company malaysian taxation 2 2. Typically, initial expense is not allowed a deduction from income of letting of continue reading →. But in malaysia, it's a bit different. Application of tax law 6.1 generally, expenses incurred by a person prior to the commencement of his operations or business would not be allowable as a deduction against the gross income of his business as they are not wholly and exclusively incurred in the production of the income. The expenses wholly and exclusively incurred in the production of the rental income are allowable as a deduction to. Expenses relating to rental of real property (pt. Generally, you are only taxed for the profit that you or your business earns. For more information and source,. For example, the cost of hiring domestic servants to help in housekeeping while one is away at work is not deductible. Although tax rates may vary based on yearly budget announcements, corporate income tax must be submitted and filed on a yearly basis, similar to an individual's personal income tax. 6.2 the following expenses incurred by a unit trust are not allowable as they Expenses of a private or domestic nature are expressly excluded from deduction; Subscriptions to associations related to the individual's profession are deductible.

But in malaysia, it's a bit different. Income attributable to a labuan business activity of the branch or subsidiary of a malaysian bank in labuan is subject to tax under the labuan business activity tax act 1990 instead of the income tax act 1967. The expenses must be incurred. Disallowable deductions expenditure which is not wholly and exclusively intended for trade purposes, is not allowable. On the chargeable income exceeding rm 600,000.

Corporate Tax Malaysia 2020 For Smes Comprehensive Guide Biztory Cloud Accounting from s3-ap-southeast-1.amazonaws.com Subscriptions to associations related to the individual's profession are deductible. Generally, repairs and renewals expenses are claimed as deductions from a person's gross income from a business or rental source. Legal fees are usually allowable and this includes costs of chasing debts defending trademarks preparing legal agreements. For more information and source, see on this link : A company or corporate, whether resident or not, is assessable on income accrued in or derived from malaysia. Chapter 5 corporate tax stds (2) 1. Application of tax law 6.1 generally, expenses incurred by a person prior to the commencement of his operations or business would not be allowable as a deduction against the gross income of his business as they are not wholly and exclusively incurred in the production of the income. A malaysian company can claim a deduction for royalties, management service fees, and interest charges paid to foreign affiliates, provided that these are made at arm's length and the relevant whts, where applicable, have been deducted and remitted to the malaysian tax authorities.

For more information and source, see on this link :

For example, the cost of hiring domestic servants to help in housekeeping while one is away at work is not deductible. Individual carrying on a business on his own. Expenses on repairs and renewals generally, repairs and renewals expenses are claimed as deductions from a person's gross income from a business or rental source. Non allowable expenses for corporation tax malaysia. Generally, repairs and renewals expenses are claimed as deductions from a person's gross income from a business or rental source. Legal fees are usually allowable and this includes costs of chasing debts defending trademarks preparing legal agreements. Tax deduction on costs for renovation and refurbishment of business premises. The advance rental would be taxed in the year of receipt. Application of tax law 6.1 generally, expenses incurred by a person prior to the commencement of his operations or business would not be allowable as a deduction against the gross income of his business as they are not wholly and exclusively incurred in the production of the income. On the first rm 600,000 chargeable income. In short, when you spend money to earn money, you're allowed to deduct that cost from the. Expenses relating to rental of real property (pt. After deducting all business losses, allowable expenses, approved donations and personal.

Related : Non Allowable Expenses For Corporation Tax Malaysia : However, the allowable expenses under subsection 33(1) of the ita is subject to specific prohibitions under subsection 39(1) of the ita..